Australia's inflation problem is home-grown

Australia's underlying inflation problem was made in Canberra and Martin Place, not Tehran.

Today is Reserve Bank of Australia (RBA) decision day. The only remaining question isn't whether the cash rate will be raised, but by how much (markets reckon 25 basis points is a given).

In the coming weeks, the Albanese government will be tempted to blame the war in Iran and higher oil prices for Australia's inflation problem. But the data tell a different story: headline CPI was already 3.8% in January, well before the first US-Israeli strikes on Iran.

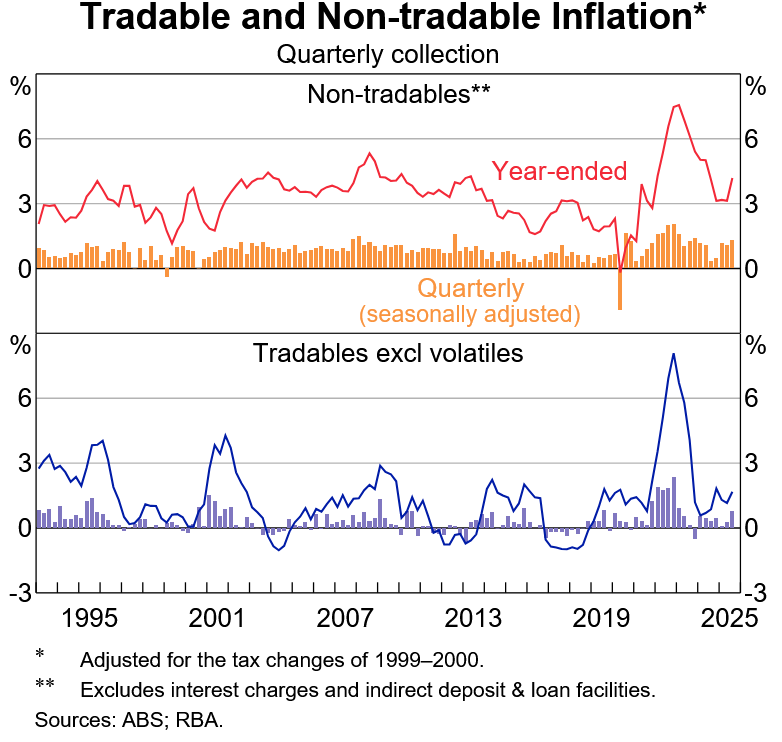

The ABS splits CPI into tradables — items exposed to international competition — and non-tradables, which are driven mainly by domestic conditions. Think rents, insurance, council rates, childcare and haircuts. It is the latter that has remained uncomfortably hot.

Oil matters for headline inflation, especially through petrol and transport-related costs. But an oil shock is a relative price shock, not a self-sustaining inflation regime. Petrol prices rise; real household purchasing power falls; other spending gets squeezed. In a credible monetary regime, that should show up mostly as a temporary rise in the price level, not a permanent lift in inflation.

The problem for the RBA is that it is confronting this shock from a weak starting position. Domestic inflation is already too high and its credibility has been dented by the inflation rebound after its premature 2025 rate cuts.

And both Governor Bullock and Deputy Governor Hauser know it. Earlier this month, Bullock told the AFR Business Summit:

"With a supply shock occurring in a situation where we already have high inflation, I think there is a risk that inflation expectations may start to move."

Hauser put it more starkly on the Grattan podcast:

"If we fail to act decisively enough to prevent inflation staying high or even rising and expectations of inflation disanchor... it will be bad for everyone... So failing to raise rates to the level they need to be and allowing inflation to get out of control is a clear problem."

The RBA is trying to claw back some of its credibility as an inflation-buster, which is essential if it's to keep inflationary expectations anchored—a task made more difficult by the government, with public spending as a share of the economy at the highest on record outside of the pandemic.

The Albanese government's instinct will be to blame Iran for everything and pressure the RBA to go easy. But that's the most dangerous possible response, and risks replicating the policy errors of the 1970s when central bankers accommodated an oil supply shock with loose policy when the underlying inflation problem was in fact domestic demand-driven. The second most dangerous response would be to use the May budget to deliver a bunch of energy subsidies or fuel excise cuts that would diminish Australia's limited reserves and help turn higher oil prices into actual inflation.

The conflict in Iran may push petrol prices higher and cause a one-off increase in the measured price level. But Australia's underlying inflation problem was (and still is) made in Canberra and Martin Place, not Tehran.