Housing's favourite villain

Australia is obsessed with taxing the supposed villains of the housing market while ignoring the restrictive zoning laws that actually lock people out.

The Australian government appears to be very keen about raising taxes on capital. Last week it was confirmed that Treasury had been instructed to investigate options, with a reduction in the capital gains tax discount from 50% to 33% "the preferred option".

It was also revealed that the government is considering capping the number of properties eligible for so-called negative gearing, otherwise known as the foundational tax principle of deducting the costs of earning an income against that income, to two.

I'm not entirely sure why the Labor government is targeting capital, specifically housing, other than through the lens of the politician's syllogism: we must do something about housing; this is something; therefore, we must do this.

It can't be just about the extra revenue, which is expected to be an estimated $5 billion a year IF applied retrospectively to all asset classes. For context, that's enough to fund the NDIS for around a month.

It might be ideology. Treasurer Chalmers idolises Mariana Mazzucato, who believes that government drives innovation yet capital owners capture the rewards while minimising their taxes.

But whatever the motivation may be, it's a bad idea.

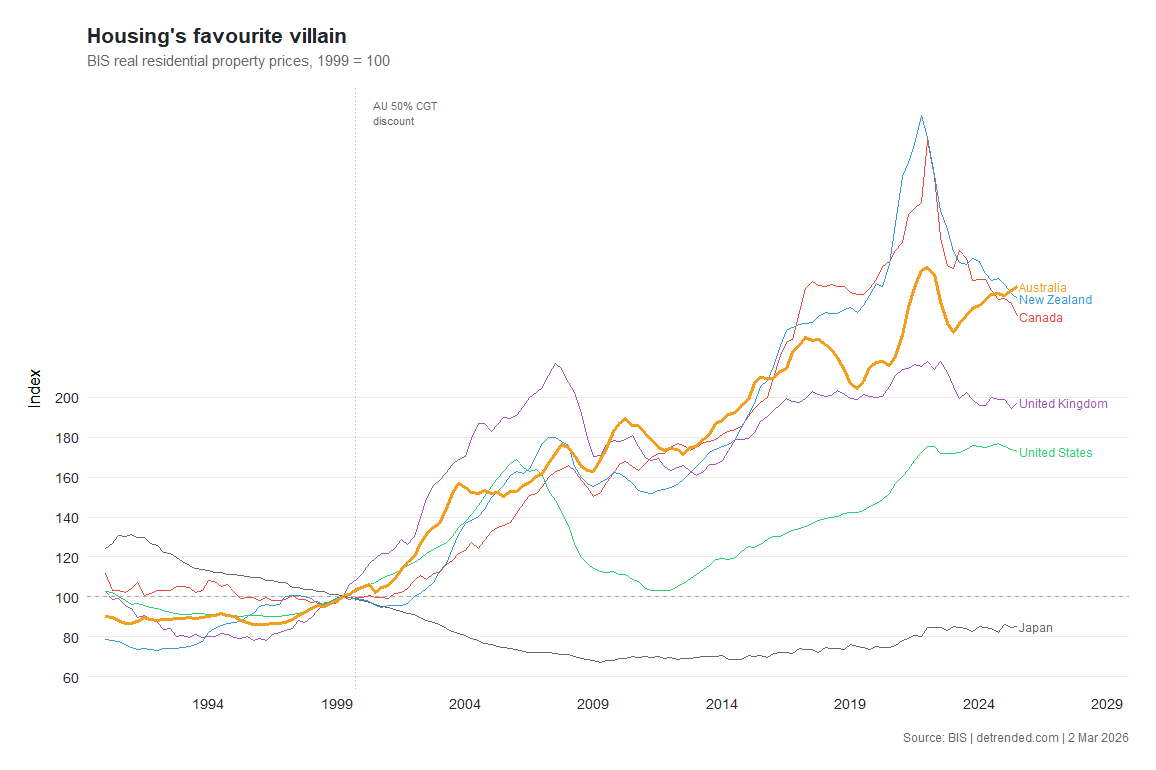

First, Australia's tax regime only has a marginal impact on housing affordability. If it was all about tax, then you would expect to see dramatically different price trajectories across countries with differing capital taxes. Yet New Zealand has no capital gains tax on property. Canada has a 50% inclusion rate that's almost identical to Australia's. The UK taxes 18-24% on housing gains. But all have experienced housing affordability crises.

The reason housing has become less affordable is supply. Specifically, restrictive land-use zoning at the state and local government levels that gum up the ability of the market to respond to demand. This isn't controversial; it's "as close to a scientific law of the housing market as we're likely to find". There's a key reason Japan is anchored to the bottom of the chart: it permits people to build.

Second, reducing the capital gains discount on housing will create a cascade of unintended consequences. Australia's rental market is one of the tightest in the OECD, and reducing the tax effectiveness (i.e. real returns) of investment property will reduce the number of properties available to rent.

Sure, a handful of people on the margin between renting and buying will tip into home ownership. But rents will rise for the rest, who tend to be on the lower side of the income and wealth ladder. The proposed two property cap for investors will have a similar effect, because small-scale landlords churn tenants much more frequently than large-scale ones, raising rental insecurity.

Third, taxes should be as neutral and predictable as possible. When your property rises in value because of inflation, that's not a real gain; it's a phantom. The 50% discount was originally introduced specifically to compensate for this, replacing a complex system of indexation. If that nominal gain is taxed, it reduces the real returns on investment, which is a distortion that changes behaviour by effectively discouraging investment relative to consumption.

Finally, it's worth remembering that the seed capital being invested has already been taxed. There's a reason a large body of economic literature argues that, under certain strong assumptions, the optimal long-run tax rate on capital is zero. That's because capital taxes compound across time in a way that labour taxes do not. In the long run that translates to more capital per worker, higher productivity, and ultimately higher real wages.

Reducing the capital gains discount would effectively discourage investment and make Australians worse off. Housing is expensive because of where it's allowed to be built, not how gains from selling them are taxed.