How not to respond to a supply shock

Allegra Spender's windfall tax idea would blunt price signals at exactly the moment you need them the most.

At the time of writing Australia's ASX200 is down 3.4% for the day, a move that follows a 1.3% decline in the US S&P500 on Friday. If futures prices are any indication, the US is in for another ~1.7% fall on Monday.

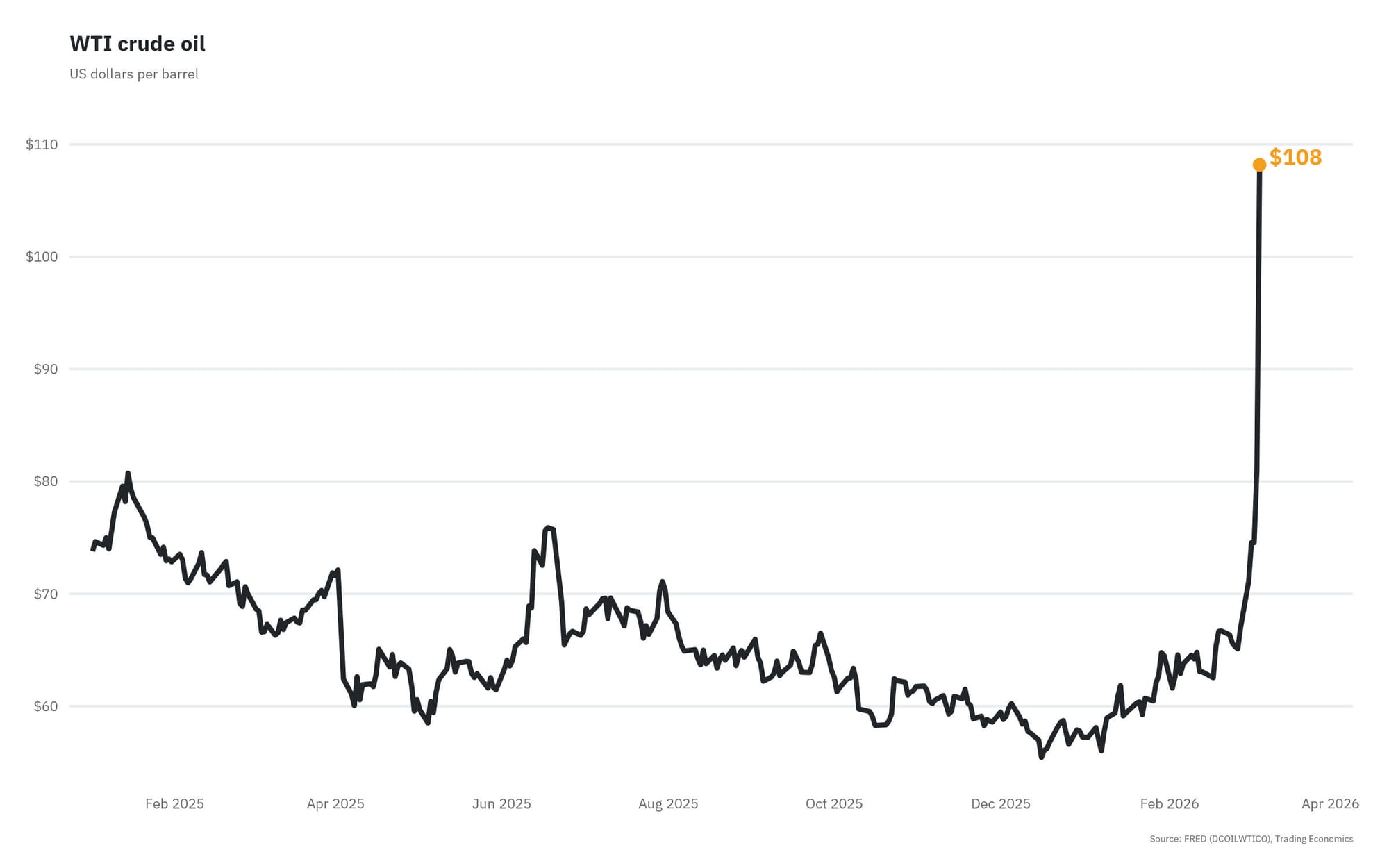

The driver of the price movements has been oil. While production has held up, the flow has slowed significantly because the carnage in the Strait of Hormuz is preventing it from getting where it needs to go: the Baltic Exchange's MEG-China TD3C freight index is up 94% since Friday. Oil prices have soared.

These are the sort of gyrations that have triggered a TACO ("Trump Always Chickens Out") moment from dear leader in the past. For as much as the average American enjoys a good, drawn-out slog in the Middle East, they don't fancy paying a premium to drive their yank tanks to the mall, nor do they appreciate paying higher prices for many other goods that use oil. As for the wealthier Americans who own the bulk of the nation's shares, well they won't be pleased at all about the events of the past few days.

Time will tell whether that happens. But in the meantime, supply shocks such as this do come with an economic cost—Westpac estimates that a three-month disruption could shave a full 0.5 percentage points off the size of the Australian economy by the end of 2026.

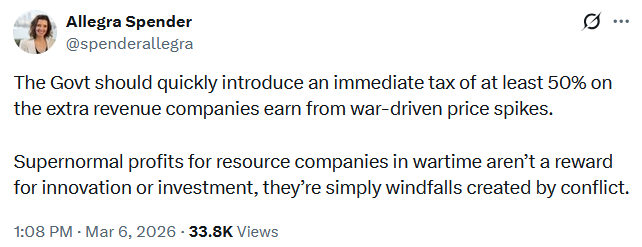

There's not much that Australia's politicians can do about that. In fact, the key with any supply disruption is generally not to make it worse: don't go around imposing price controls, or implementing knee-jerk windfall taxes to stop "resource companies" from supposedly exploiting the crisis for personal gain. Basically, don't be Teal member for Wentworth Allegra Spender:

It's intuitively appealing to want to tax "windfalls". Supply is fixed in the short run, so the price spike looks like a pure rent that can be skimmed without consequence. But that framing assumes away the entire point of prices, also known as a signal wrapped up in an incentive.

The elevated oil price (and Australian LNG, which is linked to oil) is doing three things at once. One, it's rationing scarce supply toward its highest-value uses. Two, it's incentivising consumers and firms to economise on their usage, or to find substitutes. And three, it's telling producers that the return on new investment just jumped and they should do whatever they can to bring capacity online, restart idle wells, or even explore marginal fields. A 50% tax on producers' marginal revenue blunts all three mechanisms at exactly the moment you need them most.

I have a question for Spender: will you propose a subsidy for oil and gas companies if prices crash in the future? If not, then by taxing the upside but leaving firms exposed to the downside, you will have changed the expected return on capital for gas extraction permanently. The rational response is less investment, which means even tighter supply and higher prices during the next crisis.

The political impulse to 'do something' about high oil prices is understandable. But the something that actually works is letting prices do their job.