Oil shocks don't cause inflation

The Iran war won't cause inflation unless central banks let it.

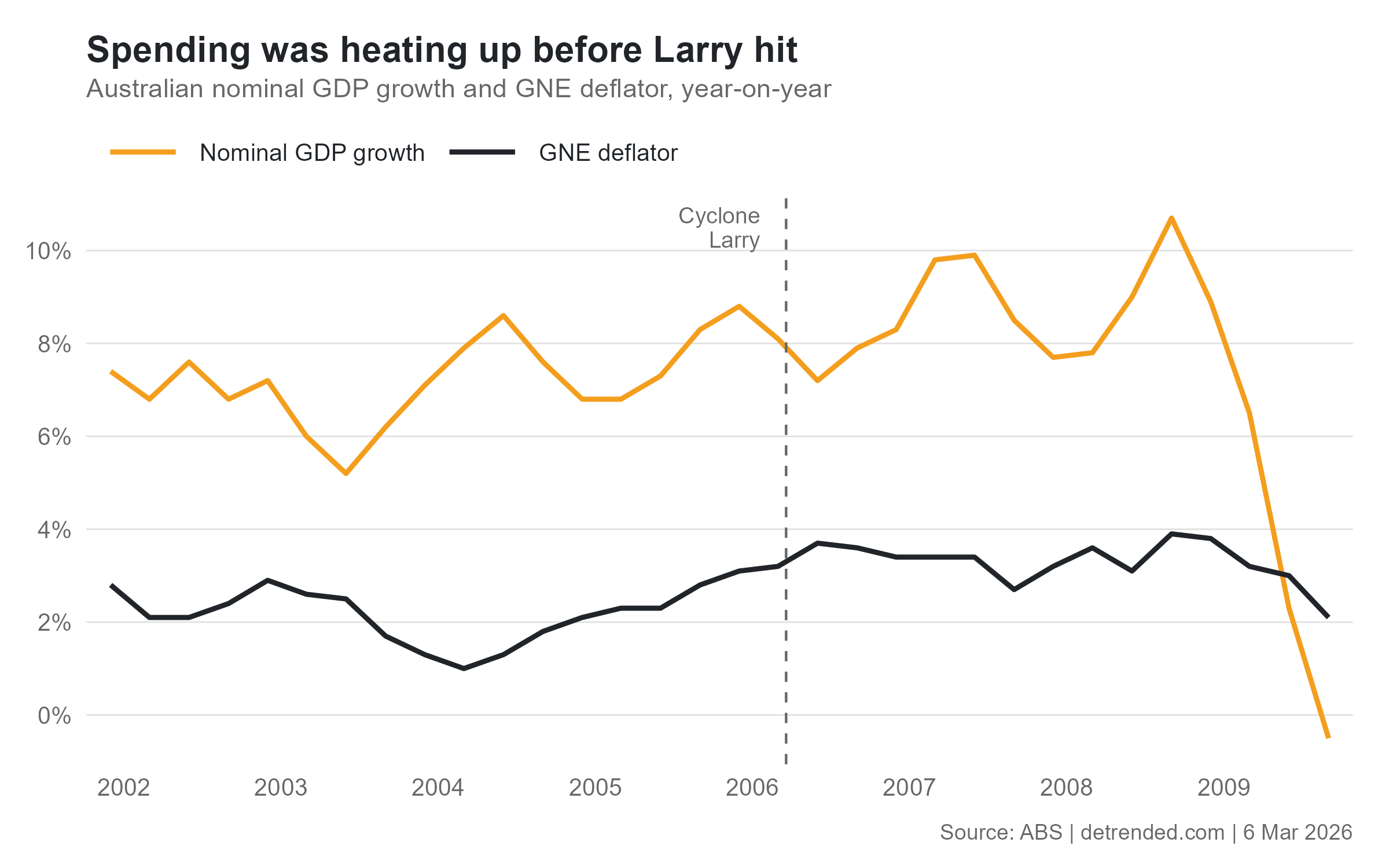

In March 2006, Cyclone Larry struck the northern Queensland coast at a place called Innisfail, the heart of Australian banana country.

At the time, politicians and even The Treasury were quick to blame the inflation that ensued on Larry:

"Inflation rose in 2005-06, partly driven by specific shocks from higher fuel prices and the effects of Cyclone Larry on fruit production and prices."

But inflation was already bubbling away behind the scenes. Nominal GDP growth, i.e. the total amount of spending in the economy, had risen from an average of around 6-7% after the dot-com bust to nearly 9% when Larry struck. And it wasn't just external factors; the gross national expenditure (GNE) deflator also started rising from around 1-2% in 2004 to 3-4% by early 2006.

Essentially, monetary policy was too easy. While the Larry banana shock inevitably affected inflation as measured by the consumer price index, it didn't actually raise inflation itself. For that to happen total spending would have to increase, enabled by an expansionary monetary policy at the RBA (to its credit, the RBA did start belatedly tightening policy shortly after the shock while acknowledging that it had to "abstract from temporary influences" such as banana prices).

Which brings me to oil prices. I was clearing my emails this morning, most of which were about the war in Iran. According to one of the Bloomberg updates, the war is "causing fear of increased loss of life, as well as deeper disruption to the oil and natural gas supply – which, in turn, threatens to unleash a wave of inflation around the world".

Will the war in Iran raise oil prices? Almost certainly. But it won't lead to inflation, defined as a sustained general increase in the price level, unless the world's central banks fail to "abstract from temporary influences" and keep nominal spending growth stable.

The price of oil is a relative price; relative to money, or to other goods and services. A higher relative price of oil means a lower relative price of other goods and services in terms of oil. Basically, a higher oil price means people can now buy either less oil or fewer other goods and services. There is no impact on inflation unless the central bank juices demand, creating the illusion that there was no supply shock by temporarily allowing people to maintain their old purchasing practices—at least until all prices start to rise, and we get another bout of inflation.

So unless Bloomberg was speculating about monetary policy – specifically, another dose of central bank monetary policy mistakes – then the war in Iran won't lead to inflation.