Sell America?

Easier said than done.

The merchant of chaos strikes again! On Tuesday, the S&P500 fell a whopping 2.06%—the most since October 2025. The US Dollar Index fell nearly 1%, 30-year US Treasury yields shot up to nearly 5%, and the gold price hit a fresh record high.

The cause was, as is often the case these days, President Trump. Over the long weekend, he tweeted an AI-generated map of Canada overlaid with an American flag, threatened escalating tariffs on eight NATO members over Greenland (read my earlier thoughts on that here), and promised 200% tariffs on French wines if they didn't join his bizarre 'Board of Peace'. When asked how far he'd go to acquire Greenland, he replied: "You'll find out."

Adding insult to injury, Danish pension fund AkademikerPension announced that it would offload all of its US Treasury holdings by the end of January, citing Trump's threats to Greenland and "rising credit risk" because US finances are no longer "sustainable".

Cue claims of a "Sell America" trade—only for Trump to fly to Davos a day later, call off his tariffs on European nations, and reassure everyone that he won't invade Greenland. The S&P500 recovered some of its losses, 30-year Treasury yields eased, and the TACO trade lived to fight another day.

Still, the brief panic is worth unpacking: is 'Sell America' even possible?

Take the Danish pension fund, AkademikerPension. It only owns around $100m in US Treasuries; a drop in the ocean in a nearly US$40-trillion market. It's also Danish, and at least until today US President Trump had been openly discussing invading a Danish territory in Greenland—a move that would be deeply unpopular with American voters (-72%), incidentally (probably why he ruled it out).

In that context, a risk-off approach is pretty reasonable. And that's before you even get to the unsustainable 7% of GDP peacetime fiscal deficit the US is currently running, which is the real story here.

But the signal is still important: when a pension fund publicly questions US creditworthiness, it's worth asking whether the premium America's bonds have enjoyed for decades is starting to reprice. Trump's chaos is the catalyst, but the underlying fiscal trajectory is what gives the concern any credibility. The price of gold is screaming risk. Sure, that doesn't mean the whole global edifice will implode tomorrow; just that the odds of it happening have gone up a bit.

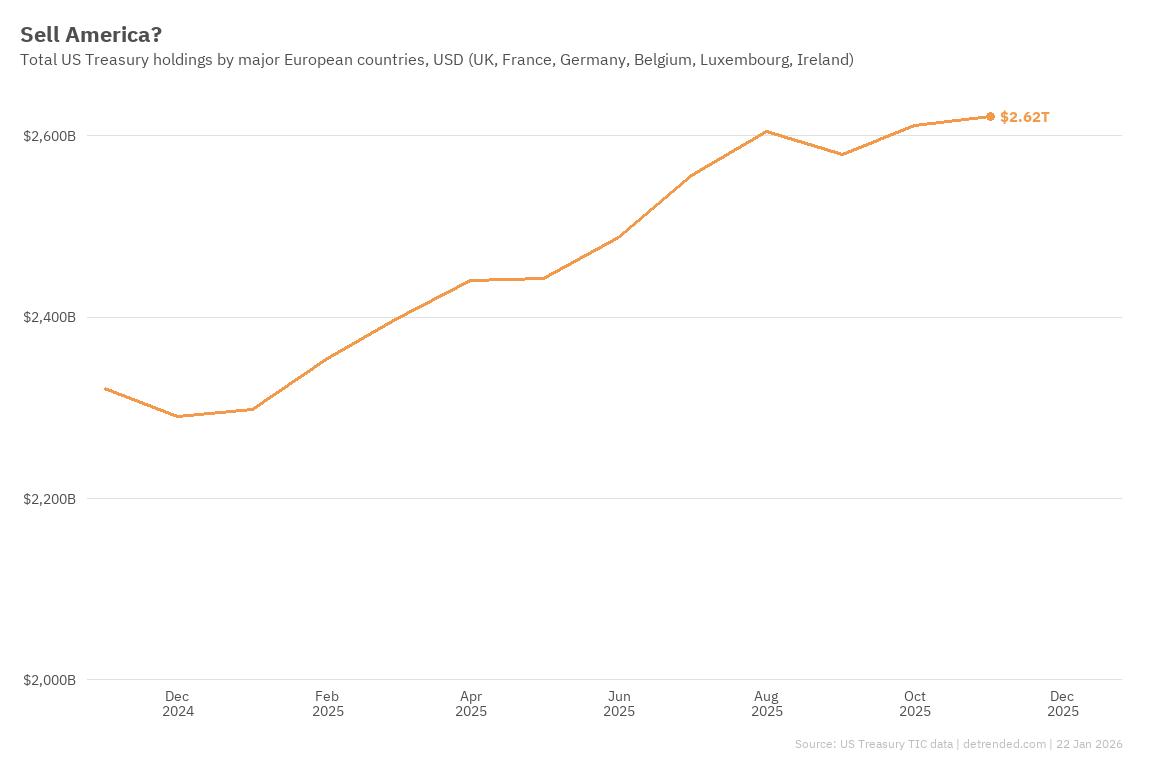

Essentially, a widespread 'Sell America' trade is just not likely. For all of its faults, the US still has strong institutions by global standards, with a reasonably functioning legislature and judiciary, the latter of which might even strike down some of Trump's tariffs in the coming days.

It's also not like other countries really have much of an alternative: some of the largest holders of US Treasuries are foreign central banks (see chart above), and they legally can't be ordered to sell. Central bank independence is still a thing in most places, and many of them hold US Treasuries for regulatory reasons that are difficult to change in a hurry. But even if they could, doing so would involve accepting huge realised losses on bonds acquired at near-zero rates just a few years ago. Their hands are effectively tied because 'Sell America' would hurt the countries flogging the debt by far more than it would hurt the US.

So as much as people might say they want to 'Sell America', in practice it's not that easy.