The capital gains tax discount is a red herring

The CGT debate is a distraction from a much harder truth: Australia's tax and transfer system is no longer fit for an aging population.

The Greens-led inquiry into Australia's capital gains tax discount (CGT) concluded this week. It made four findings that were relatively ambiguous, such as that it "can distort decision making and incentivise tax planning", so I'm not sure how influential it will be with the Albanese government. The reason it shouldn't be influential is because its findings could be said about virtually any tax, given that by definition taxes distort behaviour and have "the potential to distort the allocation of investment across the economy".

The most specific "finding" was the third, which claimed that "the concessions provided by the capital gains tax discount, in combination with negative gearing, have skewed the ownership of housing away from owner-occupiers and towards investors".

But notice the bait and switch: the CGT is no longer "distorting" behaviour; it has simply "skewed" housing toward investors. That's because the tax distortions in the housing market predominately go in the other direction, with the Treasury-calculated "concessions" for home owners dwarfing those for investors.

What the Greens' inquiry did get right was that it's important when designing tax policy to minimise distortions. The CGT discount exists as a crude method of doing exactly that by providing compensation for inflation: without it, Australia would overtax all capital (savings and investment) by more than it already does and end up with a lot less of it.

Given that capital investment is strongly correlated with long-run productivity and real wages, that wouldn't be a good thing!

But the real problem with the Albanese government's CGT obsession and its supposed focus on "intergenerational inequality" is that it ignores where the imbalance actually comes from: spending.

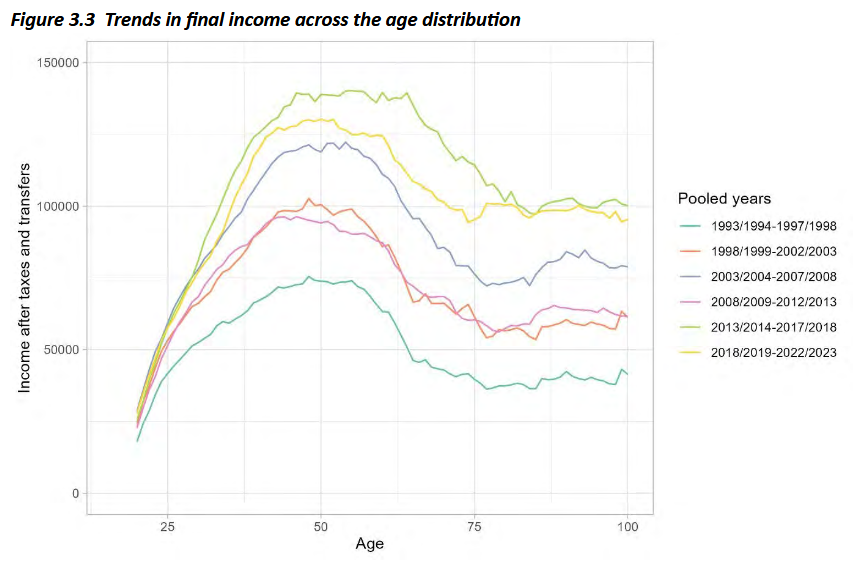

An ANU paper from May last year presented at an RBA conference quantifies the shift. Total government expenditure is increasingly targeting older Australians via automatic spending through the age pension, aged care and health. That by itself would be a problem in an aging society such as Australia's. But over the past three decades it has gone far beyond that, with spending increasing significantly in real, per-person terms, while transfers to younger cohorts have barely moved.

In the early years of the study (1993-94 to 2002-03), Australians over 60 had after-tax income equal to 61% of working-age Australians. In the most recent decade, that figure hit 95%. Compared to 18-30 year olds specifically, over-60s now earn after-tax incomes around 60% higher.

The CGT discount is a red herring; Australia's real issue is government spending. Not just the total amount, which is at all-time highs as a share of the economy, but where that spending is happening.

You don't get wealthy by dividing the pie but by growing it. Tax and transfers are essential for any healthy democracy, but there are limits. Cutting the CGT discount will move the dial further in the wrong direction: if applied to all capital it will disincentivise saving and investment and therefore productivity; if only to housing it will drive rents up as housing investors increasingly decide it's not worth the hassle.

The paper's authors put it plainly: the tax and transfer system has not adjusted to the changing age profile of income in Australia. Only about two-thirds of household income even enters the personal income tax base, with superannuation and owner-occupied housing largely excluded (Treasurer Chalmers already made an absolute hash attempting to tax the former).

Yet the government's proposed solution to a system that under-taxes older Australians is to raise a tax that primarily hits working-age investors, both because they're most active in buying investment properties and because they tend to have more labour income to which capital gains are added.

The real villain isn't the CGT discount. It's the spending.