The precious metals crash

Gold had its worst day since 1983. Silver fell 30%. Every outlet blamed Trump's Fed pick. But the data tell a different story.

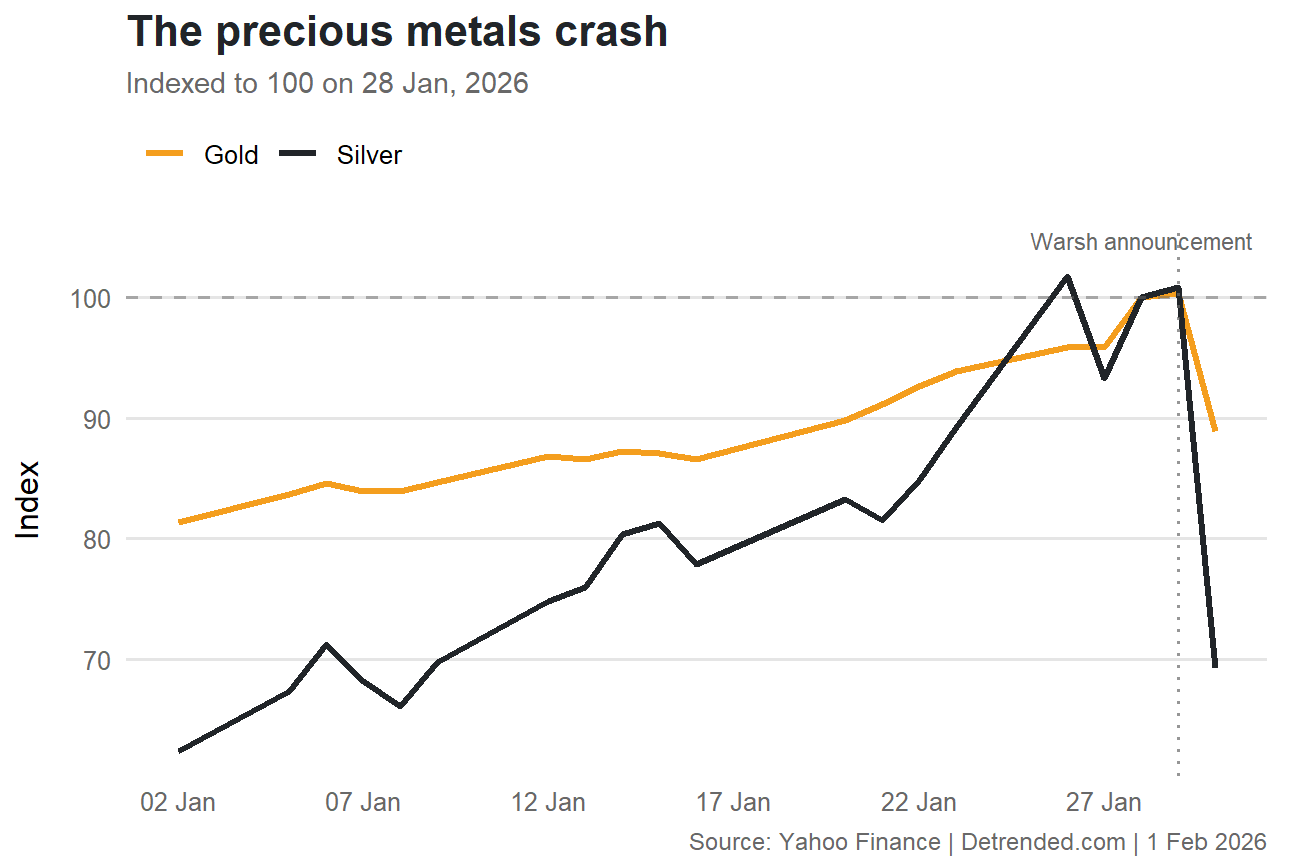

There was chaos in the precious metals market at the end of last week, with gold finally ending what has been a remarkable run with its worst day since 1983, while silver fell nearly 30%—its worst trading day ever.

Nearly every financial news outlet ran with a similar headline: Trump's Fed chair pick, Kevin Warsh, sent precious metal prices crashing because of his "hawkish" views on monetary policy.

First, some context: gold has been on a tear in recent months, riding high on trade war hedging, geopolitical uncertainty, and sustained central bank buying. Oh and US President Donald Trump, who has been talking down the US dollar and publicly calling for lower interest rates, potentially undermining the independence and therefore credibility of the central bank as an inflation fighter.

Put it all together and January was the best month for gold since 1999, even with the last-day crash.

That changed when Trump nominated Warsh; not necessarily because Warsh is a monetary "hawk" as has been reported, just that he's probably not going to be as "dovish" as some of the other candidates Trump was considering, such as Kevin Hassett. Prior to Warsh's nomination prediction markets only had his odds at around 25%, so the other outcomes were inevitably priced into precious metals, and were promptly reversed.

But there's also a bit more to this than meets the eye.

One, if gold crashed on Fed policy repricing alone, we'd expect to see similarly large moves in other markets. And while the US dollar did strengthen, Treasury yields were broadly flat, while silver got destroyed.

Two, another move affecting precious metals arguably happened at the same time on the other side of the Pacific: China's regulators suspended trading in five commodity ETFs, explicitly targeting silver and oil funds.

Chinese retail investors are massive participants in commodity markets, including precious metals. These ETFs represent a significant demand channel, with China being the world's largest gold and silver market. When regulators suspended them to "curb investment mania", they raised the risks of holding precious metals relative to other assets, taking the heat out of demand and therefore prices.

Basically, if the gold and silver price declines were purely about Warsh's confirmation, both gold and silver should have moved together, and bond yields should have lifted reflecting expectations for tighter monetary policy.

Neither happened.

Warsh, whatever his actual policy views, has genuine intellectual credibility and central banking experience. His nomination likely shaved a few percentage points off gold by reducing some of the Weimar Republic inflationary tail risk that had supported prices. But attributing the entire move to Warsh requires ignoring China's regulatory intervention, the silver/gold divergence, and flat Treasury yields.