The RBA is losing the war on credibility

The RBA spent 2025 fuelling a fire it now lacks the credibility to extinguish.

The ABS released February's monthly CPI today. It was a relatively benign data point: annual inflation was down 0.1 percentage points from January to 3.7%, while trimmed mean – which strips out volatile items and is therefore a better indicator of future inflation (what truly matters for policy) – was unchanged at 3.3%.

But whatever the number, it almost certainly understates the pressure in the pipeline because the reference period pre-dates the Iran oil shock entirely.

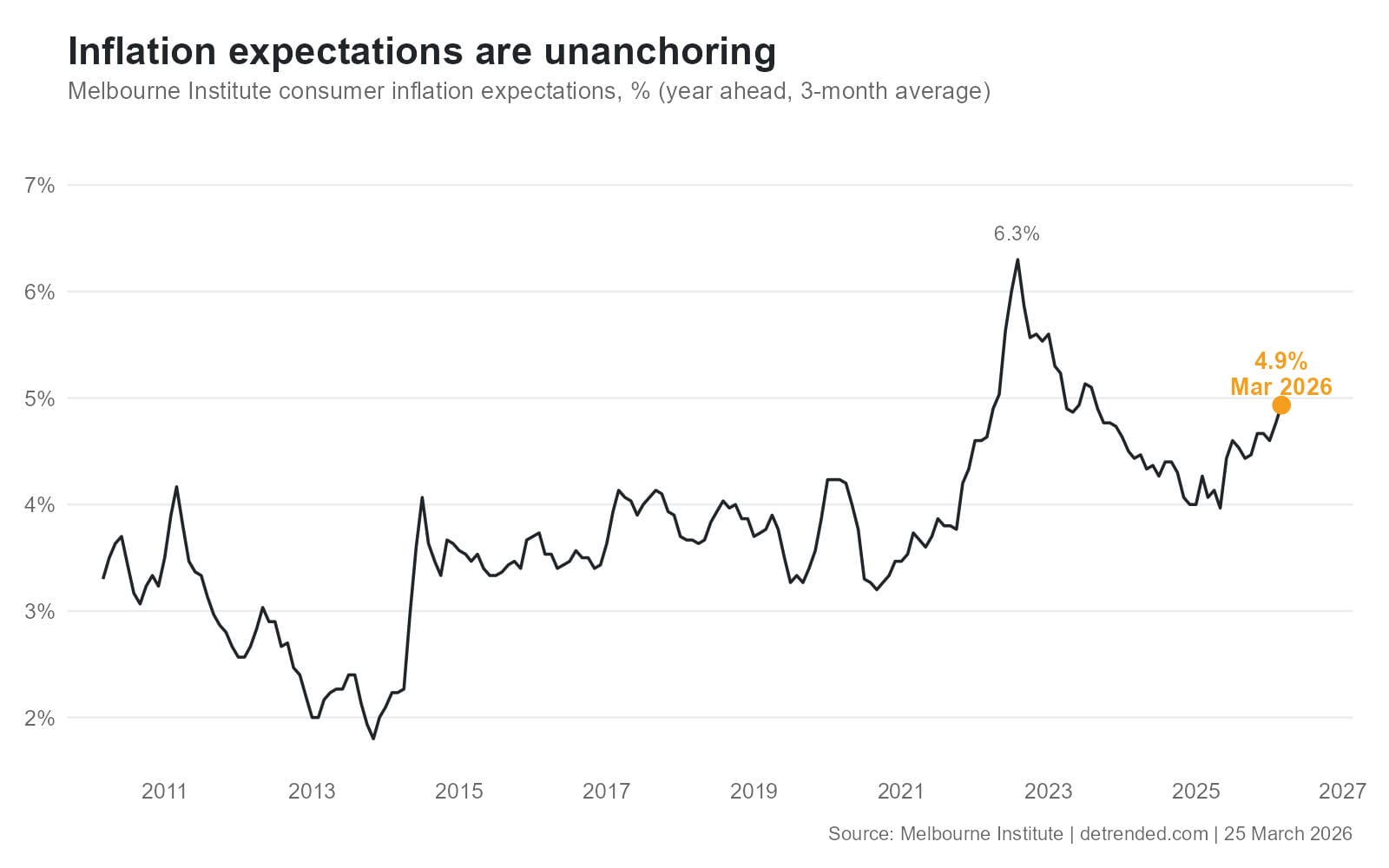

Thankfully there are forward-looking alternatives. The Melbourne Institute's consumer inflation expectations hit 5.2% in March, the highest since July 2023. ANZ-Roy Morgan's weekly measure is even worse: 6.9% in mid-March, a jump of 1.6 percentage points in just a few weeks as petrol prices surged. Google Trends data for "inflation" searches in Australia are at their highest since mid-2023, when measured inflation was still running above 6%.

This matters enormously for monetary policy. As monetary economist David Beckworth argued yesterday, a central bank with established credibility can afford to "look through" supply shocks. Keep policy steady, let the temporary price spike pass, and trust that expectations stay anchored. But when expectations are already fragile, even a temporary shock can dislodge them, and the central bank gets forced to tighten into an already weakened economy. The result is worse outcomes on both sides of the mandate: more inflation, less growth, and therefore higher unemployment.

That is precisely the pickle the Reserve Bank of Australia (RBA) is now in, and it has nobody to blame but itself.

The RBA spent most of 2025 prioritising the employment side of its dual mandate, attempting to walk the "narrow path" of bringing inflation back to the 2-3% target range without triggering a recession or substantial unemployment. So when it appeared that inflation was starting to cool, it was quick to ease monetary policy even as proxies for total spending, such as the GNE deflator, were running hot. By the time the Board reversed course in February 2026, headline CPI had already doubled from its June trough of 1.9% to 3.8%. The two hikes since then, including a narrow 5-4 vote in March, have only just begun to undo the damage.

The cruel irony is that by prioritising employment in the short run, the RBA may end up delivering worse long-run outcomes on both the inflation and employment fronts. With expectations unanchoring, the Board cannot simply "look through" the oil shock and wait for it to pass. It will likely have to keep monetary policy relatively tight even as higher energy costs sap real household incomes and dampen growth, leading to higher unemployment than would have been necessary if it had used the past two years to restore its inflation-fighting credibility.