The next reform victim

The Albanese government has found its next target, don't bank on a rate cut in 2026, and no matter how bad it gets there's always the UK.

Like a plague of locusts looking for the next bountiful crop to sink their teeth into, the Albanese government has apparently set its sights on "reforming" the next juicy target: artificial intelligence. Speaking to CEDA, Albo said:

"We can bring our national values of fairness and opportunity to AI, so that it grows our economy and strengthens our sovereignty, without fragmenting our society or damaging our environment."

That sounds good in the same way that land-use regulations sounded good in the 70s and 80s, with a consequence being today's lack of affordable housing. Policy making is all about trade-offs, and it's rare that you can have everything.

Do you want your country to be a world leader at using AI, or do you want AI sovereignty? In a small, open country like Australia, these are almost certainly incompatible goals. No matter how many data centres you build in Australia, the top model weights will be closed and foreign-owned. You could run open source models, or subsidise the development of Bruce AI locally, but then you wouldn't be a world leader, would you?

Do you want to preserve the existing environment and patterns of exchange, or allow people to freely innovate and exploit AI opportunities, even if that means more resources going to data centres? If you want to grow the economy, you also have to be prepared to pay the political bill that comes with it. That might mean higher consumer prices in the short-term, followed by more public spending on infrastructure, given that energy and water utilities have high amounts of government involvement. But you can't have one without the other.

The key isn't pretending that there are no trade-offs, but getting the rules of the game right; ensuring Australia has the institutional settings that maximise the net benefits for society, even if that comes with perceived costs in terms of highly subjective values such as "fairness".

Given his previous approaches to speech (e.g. the Orwellian under 16 social media ban that hasn't worked) and free exchange (e.g. Future Made in Australia; capital gains tax changes), I'm almost certain that is not what Albo has in mind.

Don't bank on a rate cut

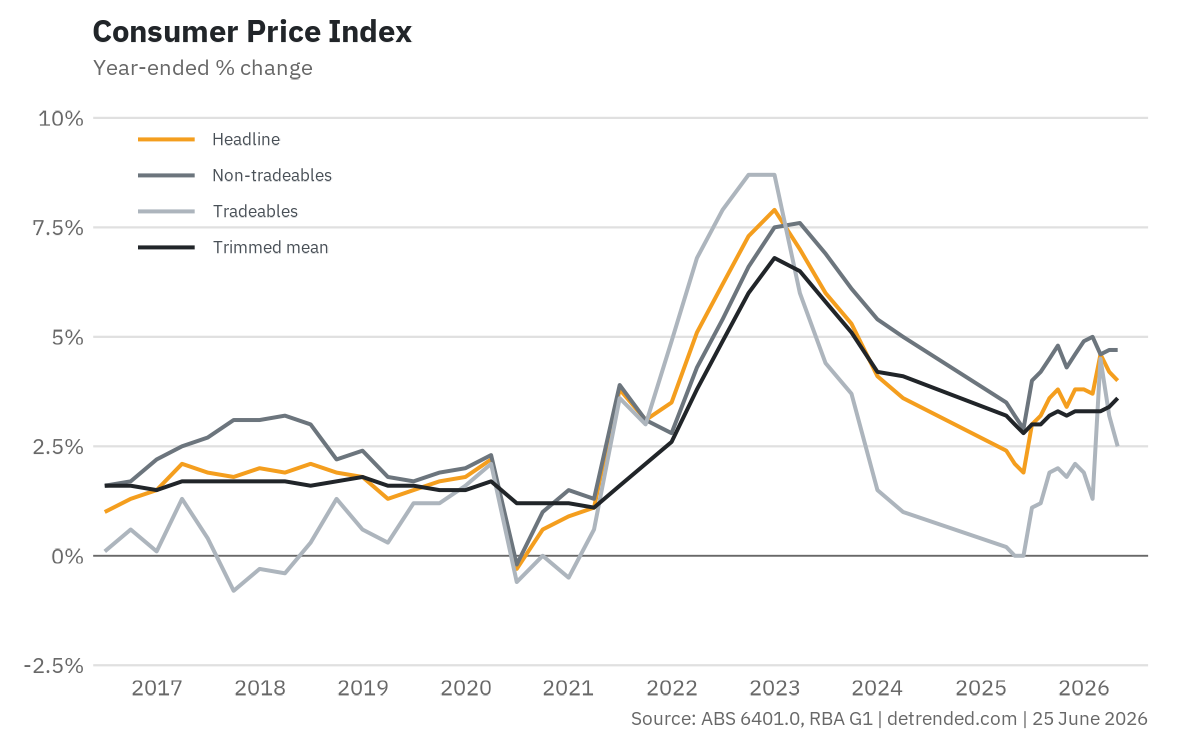

Quite a few bits of key Australian data were released this week, including the CPI, household spending, and employment. All three will have been concerning for the RBA, given they unanimously suggest that domestic demand is still running a bit too hot.

Take the CPI. While Treasurer Chalmers tried to gaslight the public into thinking inflation had cooled in May, the slowdown in the headline figure from 4.2% to 4.0% was largely due to "the impacts of the halving of the fuel excise on 1 April".

A better gauge of where inflation is at is the trimmed mean measure, which strips out volatile items such as fuel. That increased to 3.6%, from 3.4% last month, and the rising trend is what's uncomfortable. You can only hide inflation for so long using handouts, which ultimately just delay (and worsen) the inevitable rise in measured inflation.

Perhaps, then, it shouldn't come as a surprise that despite crude oil prices now back close to pre-Iran war levels, the Albanese government decided to extend the fuel excise cut for another month at an estimated cost of $400m. Just imagine how bad inflation might look if the government wasn't still actively manipulating it!

Moving to employment, May was a solid month for the labour market, which is great news for workers but again spells trouble for the RBA: a resilient labour market along with elevated spending and persistent above-target inflation suggests that the RBA might have monetary conditions set a bit too loose. And spending was indeed uncomfortably high in May, with the nominal household spending indicator showing a broad increase across all spending categories.

I don't envy the RBA; dealing with the effects of what's likely to be a temporary, external shock while inflation is already elevated is close to a worst-case scenario. But it's also exactly why it's so important to stay on top of inflation and anchor expectations in the first place, so it's hard to feel much sympathy for those running the show, most of whom have been in their roles for many years now.

It could be worse

For all the less-than-ideal political decisions seemingly being made in Australia, just remember that it could always be worse. We could be the UK, where they've just ousted their sixth Prime Minister in a decade (the seven prior to that lasted 46 years).

It's not like it's going to get any better, either. Outgoing Labour PM Keir Starmer looks set to be replaced by Andy Burnham, who – like Boris Johnson, one of the six he's replacing – is a popular but untested former mayor who just won the by-election that spelled the end for Starmer. In terms of policy, Burnham plans to unleash what he calls "business friendly socialism" on the country, which includes nationalising industries across energy, water, and transport, and legislating to make it a "human right" to have a "good, secure home".

None of that will be cheap, let alone efficient. Meanwhile, the UK's net public debt has nearly tripled since the mid-2000s and is set to pass £3 trillion, or nearly 100% of GDP, within the current budgeting period.

Have a great rest of your weekend.