Australia's coming inflation

The Strait of Hormuz delivered the price shock. Whether it becomes inflation is up to Canberra and Martin Place.

The ABS will release Australia's consumer price index (CPI) figures for March tomorrow. The war in Iran started at the end of February, so it'll be the first full month affected by the closure of the Strait of Hormuz.

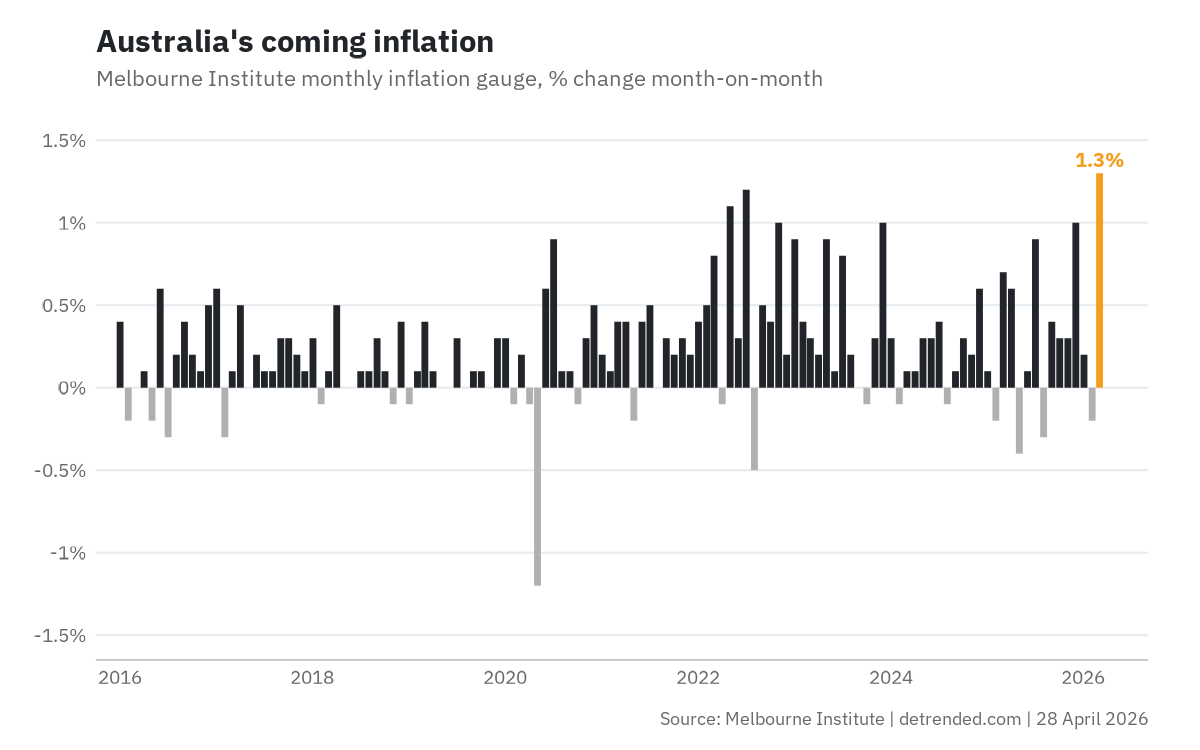

We already have a taste of what's to come. The Melbourne Institute's inflation gauge jumped 1.3% in March, the largest monthly increase in the series' history. Such large jumps probably won't last given how rapidly fuel prices responded to the closure, but as that feeds into other prices it'll inevitably keep measured inflation elevated for at least several months.

Note the important distinction. The rise in prices is measured as inflation (CPI), but actual inflation – defined as a sustained increase in general prices – doesn't necessarily have to follow. Prices rise once because of the oil supply shock and then settle at a higher level, with the rate of inflation gradually falling back to where it was before the shock.

The higher prices are signalling that Australians have become poorer. The real risk is that Australia's institutions react in the wrong way, responding with policy that makes everyone even worse off.

For example, will the RBA hold the line and continue lifting interest rates, even as higher fuel prices lead to demand destruction? Raising rates into an oil shock is usually a mistake. But actual inflationary pressures in Australia were running hot well prior to this crisis, so the RBA doesn't have the luxury of other central banks in being able to hold its hands up and tell people it will simply 'look through' the full impact of the shock.

Will Australia's state and federal politicians be able to resist the siren song of the unions and other interest groups, who are always eager to turn a temporary supply shock into a more permanent demand shock? The Fair Work Commission makes its annual wage decision in late May or early June (affecting roughly half the workforce), with the ACTU pushing for a 5% rise and the Albanese government effectively endorsing it. Inflation as measured by the headline CPI may well be printing north of 4% by then, so the political pressure to do something will be considerable.

The labour market clears on two primary margins: wages and employment. If the former rises without a commensurate lift in productivity, the latter adjusts to clear the market. The alternative is the RBA accommodates the wage rise with looser policy, in which case the adjustment comes through inflation instead.

Ultimately, lifting wages in response to the oil shock only shifts who bears the cost, with the added risk of embedding the price increase into the wage-setting system in every round thereafter. If those expectations get baked in, the result is usually some combination of higher inflation, higher mortgage rates, and higher unemployment, depending on the magnitude and timing of the RBA's response.

The uncomfortable truth is the oil shock has made Australians poorer by raising the cost of everything that moves. If the country wants to avoid even worse outcomes, then some tough decisions are going to have to be made. Tomorrow's CPI print marks the beginning of a politically challenging period that will run through the June quarter and beyond.