Why markets didn't react to Australia's budget

The most controversial budget since 1993, and the bond market didn't bat an eye.

I'm not sure there has been an Australian budget as controversial as last week's in many years (according to Newspoll, not since 1993). I've certainly never seen this kind of media reaction, with pundits rightly pointing to various inconsistencies and potentially serious unintended consequences.

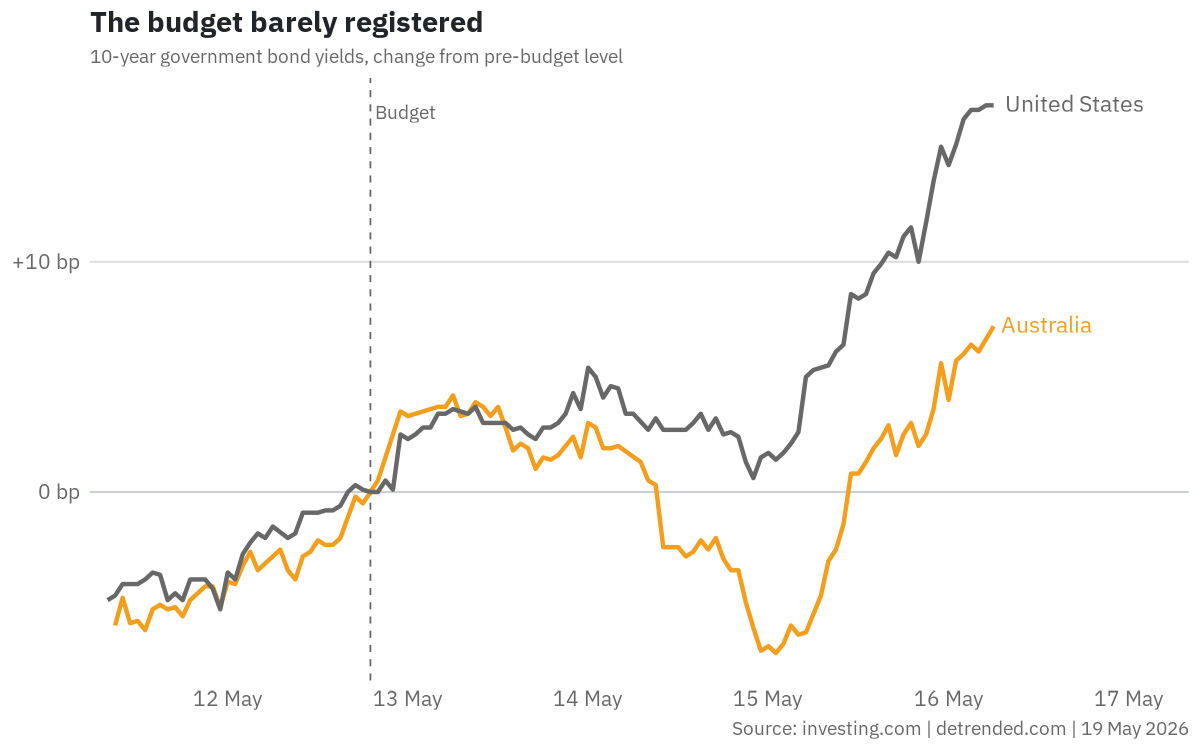

But for all the outrage, some justified and some not-so much, markets barely budged. As Treasurer Chalmers spoke, Australia's 10-year bond yield ticked up a few basis points. But that was it; and it wasn't even unique to Australia. For the entire week the Australian 10-year and the US 10-year moved almost in unison, even on budget day. There's no obvious Australian dislocation; no gap opening between the orange line and the grey one until well after the budget was revealed. Basically, Australia's bond market was trading world events rather than local ones, the same as it does every other day.

For such a controversial budget, the obvious question becomes: why? There are a few possible explanations.

One, almost nothing actually announced on budget night was entirely new: the major measures had been leaked or announced over the preceding weeks, dribbled out through the press or pre-released in ministerial pressers. A bond market prices news when it arrives, not when it's formally read into Hansard. By the time Chalmers stood up, the substantive content had already been absorbed over the preceding month, so there wasn't much left to price in.

Two, a budget is not enacted policy. To become law it still has to clear the Senate, and Labor's numbers leave only two routes to a majority: working with the Greens or the Coalition. Lean on the Greens and the price of their votes is a budget pushed further from anything a market would applaud. Think the backlash to the budget was bad? Wait until you see what the Greens will demand to support it. As for the Coalition, given the budget reply effectively said it would oppose all the tax changes in their entirety, that seems unlikely.

Regardless of the route eventually taken, the bond market is pricing the range of things the budget might become after the legislative sausage is made, and the centre of that range is perhaps milder than Chalmers' speech, especially given the public backlash (above all else, Labor wants to win the next election).

Three, the budget might have landed softly because of where it sits relative to the rest of the world. It added to debt and entrenched structural spending, to be sure, but the numbers aren't as bad as everyone else's. On a planet of fiscal incontinence, being merely irresponsible is a competitive advantage.

In times like this I'm always reminded of the great economist Adam Smith, who when British MP John Sinclair wrote to him fearing that defeat in the American war would leave Britain "ruined", Smith replied "Be assured, my young friend, that there is a great deal of ruin in a nation."

On balance the budget was a bad one, but it wasn't even close to breaking the world's 12th-largest economy. At least not yet; the sustainability of Australia's fiscal path relies heavily on commodity prices staying elevated and that proposed cuts to growth in the NDIS are actually executed. But everything is relative, and the bond market doesn't care about political ideology. Nations can absorb a remarkable amount of bad policy before the day of reckoning arrives, and the bond vigilantes haven't come for Australia because for all the ruin, there's still plenty to like relative to what else is out there.