Canada's borrowed wealth

Canada might be getting a sovereign wealth fund. Whether Canadians ever get any wealth out of it is a different question.

Earlier this week, Canada's Prime Minister Mark Carney announced the creation of Canada's first sovereign wealth fund. Called the Canada Strong Fund, it's going to get an initial $25 billion federal contribution to invest in "clean and conventional energy, critical minerals, agriculture, and infrastructure", with returns reinvested and a retail investment product to follow.

I'm generally a fan of sovereign wealth funds, but only under the right conditions. The problem with Carney's fund is it doesn't meet any of them.

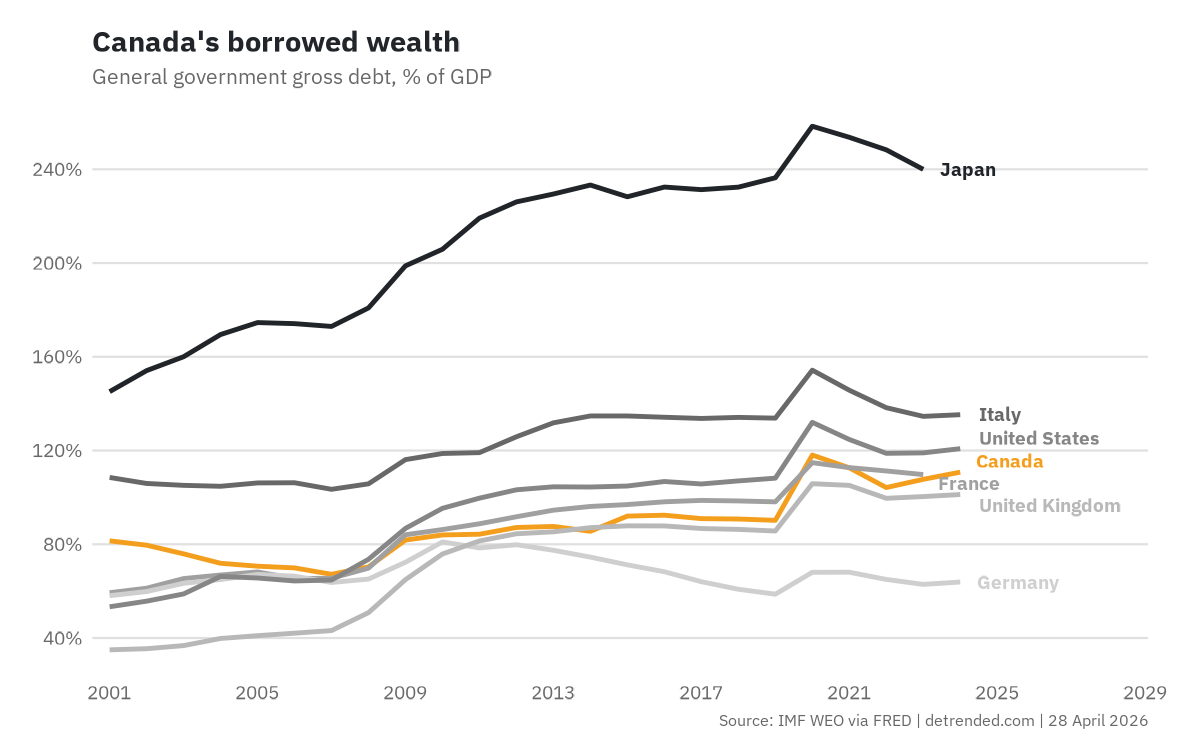

Let's start with the fact that Canada doesn't have $25 billion lying around. The government likes to claim it has the lowest net debt in the G7, which is true only if you count the Canada Pension Plan and Quebec Pension Plan as usable assets. I don't know about you, but ripping away the funds explicitly owed to current and future pensioners to pay off the debt seems like it would be politically impossible.

A more accurate figure is gross debt, which at around 110% of GDP is the fifth-highest in the G7. And it's not getting any better; the federal government expects to have run a deficit of 2.5% for the year ending March 2026, and the Parliamentary Budget Officer expects the federal debt ratio to keep drifting upward through the end of the decade.

That alone should be enough to preclude a sovereign wealth fund for Canada. The world's most well-regarded sovereign wealth funds were built with equity, not debt. Norway's Government Pension Fund Global, for example, is funded by oil revenue and the government runs structural budget surpluses. Singapore's GIC and Temasek sit alongside reserves grown over decades of consistent fiscal surpluses; Singapore has no net debt.

Now, there is a case for a government borrowing to invest, even in stocks. Equities earn more than government bonds, so a well-managed, debt-financed fund could in principle be in the nation's interest. But stocks are volatile, and the equity premium only exists because of that extra risk. Every borrowed dollar inside the Canada Strong Fund is a dollar a Canadian could be spending or investing, or the federal government could be using to retire debt and lower future tax bills.

But arguably the bigger problem with Carney's fund is what follows once the government starts taking equity stakes in domestic firms. Both Norway and Singapore invest predominantly in foreign assets (Norway's is zero by rule), partly to diversify and partly to avoid distorting their own economies.

The Canada Strong Fund might earn perfectly respectable returns by investing in Canada. But state-backed firms tend to lobby for favourable regulation, tax treatment, and procurement contracts. Their competitors, knowing they can't out-lobby Ottawa, invest less. Capital allocation across the economy starts answering to political objectives instead of price signals. Productivity and dynamism fall, meaning the Fund itself can look like a winner while the economy around it loses.

Carney's announcement makes this worse, not better. By restricting the Fund's investment universe to "clean and conventional energy, critical minerals, agriculture, and infrastructure", he's pre-committing it to picking domestic projects in politically chosen sectors, the same sectors already covered by the Canada Infrastructure Bank, the Canada Growth Fund, and Export Development Canada. It's politically captured from the very beginning.

Canada might be getting a sovereign wealth fund. Whether Canadians ever get any wealth out of it is a different question.