Low debt buys you optionality

Australia has been burning its fiscal buffers in the good times, leaving it with little in the tank for the next real crisis.

I'm in Hong Kong and Singapore for the next week so posting will be light, if at all. If you'd like to catch up, let me know!

Australia's next federal Budget is due on 12 May. I don't know what's going to be in there—it's being framed as an "intergenerational equity" Budget, so probably a bunch of what I'd call reform theatre; or changes that sound like they'll tackle various social hotspots head-on, but in reality will only have a marginal impact because they completely ignore the actual drivers of those issues.

But what I do know is that despite temporary revenue tailwinds from the wars in Ukraine and Iran (Australia is a large commodity exporter and has one of the world's highest federal company tax rates), the Budget will almost certainly do nothing to address the structural fiscal deficit. And the longer that continues, the more fragile Australia will become.

For most of the last decade, the elite consensus was that government debt didn't really matter. Rates were at or close to zero, inflation was dead, and any economist who fretted about deficits was waved away as a crank.

That argument is ageing badly.

Global public debt hit 93.9% of GDP in 2025, and the IMF now expects it to breach 100% by 2028. Japan, the supposed proof that debt doesn't bite, is now the cautionary tale. Long yields are climbing, the yen is sliding, and the Bank of Japan is stuck with a choice it spent twenty years pretending it would never have to make: accept higher debt servicing costs or let inflation run. There's now a very real risk that the Japanese public sector, which has been operating as something akin to a sovereign hedge fund for decades by saddling its taxpayers with risk to earn excess returns, could see its funding costs rise and suffer serious capital losses.

There's also a growing body of work that shows, actually, too much debt is bad after all. For example, a recent journal article in the Oxford Economic Papers looked at manufacturing industries across advanced economies since 1980 and found that high public debt predicted a disproportionate and persistent slowdown in R&D-intensive industries. Firms in innovation-heavy sectors cut back on research when government debt is high, plausibly because policy uncertainty rises and financing frictions bite harder. High debt eats away at next year's budget through interest repayments and crowds out the productivity frontier, on top of the usual trade-off against higher long-run risk.

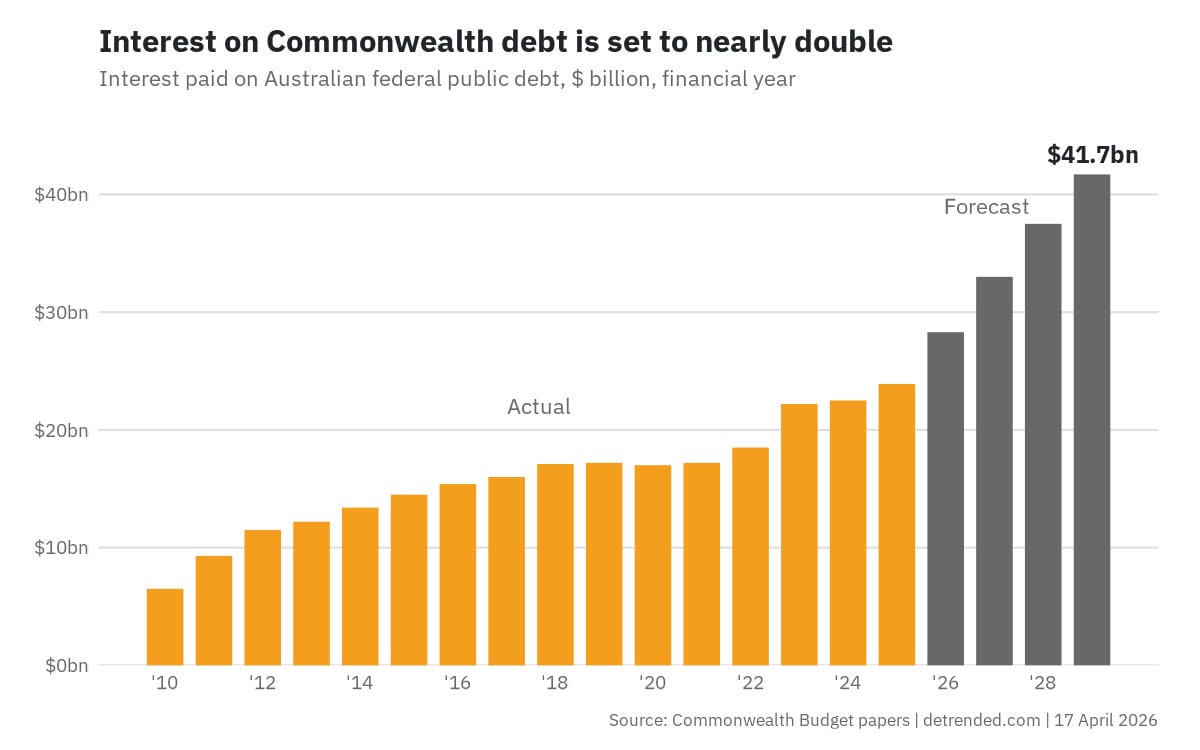

Fortunately for Australia, public debt is modest by OECD standards. But it has been growing quickly, along with the interest bill. Federal debt servicing costs have climbed from around $6bn in 2009-10 to $24bn last year, and could double again by the end of the decade, making it the fifth-largest line item in the federal budget. That's money the government is obliged to hand to bondholders before it spends a dollar on anything voters might actually want.

David Morgan, one of Paul Keating's lieutenants from the reform era, made the point earlier this month that low debt buys you optionality when a shock arrives. You can respond to an oil crisis, a pandemic, or a war without flinching at the bond market. But run the buffer down in good times, as Australia has been doing, and you have nothing left in the tank when it matters.

Unfortunately, the Albanese government has continued and accelerated that trend. Public spending as a share of GDP is at all-time highs, and flagship policies such as a Future Made in Australia are old-school industrial policy financed with yet more debt. He might pitch it as growing the nation's resilience, but the outcome will be the opposite: debt-financed subsidies to politically favoured sectors, crowding out the private investment that would otherwise lift productivity, while leaving less fiscal room for the next actual crisis.

I hope that the next Budget proves me wrong, and Albanese and his lieutenant Treasurer Chalmers actually do something to address the structural fiscal deficit. But I'm not going to be holding my breath.