The housing wealth illusion

Australia's $12.3 trillion housing stock isn't a pool of misallocated capital, but a mark-to-market valuation of a policy-induced supply constraint.

Last Friday evening the ABC published some commentary on a new business podcast it launched hosted by Alan Kohler. For those not familiar with Australian media, Kohler has been gracing the pages of local newspapers since the early 1990s. He has no formal economics training so has a tendency to make the odd basic error, such as thinking foreign students should be an import in the national accounts (they're an export, for good reasons), or that John Howard's introduction of a capital gains discount to replace the cost-base indexation system is responsible for Australia's high house prices, despite prices also rising in countries that didn't change tax regimes.

Given Kohler has written a book on Australia's "housing mess", it was no surprise that he peppered his guest, Paul Schroder (chief executive of AustralianSuper) with housing-related questions, to which he got some interesting answers:

"[Schroder] said Australia needed to have a serious conversation about its capital allocation, because the inflated level of our housing wealth was extreme compared to the size of our economy.

He said the nominal value of gross domestic product (GDP) in the United States is US$31.4 trillion and the value of US housing stock is US$55 trillion.

By comparison, Australia's GDP is worth $2.7 trillion and its housing stock is worth $12.3 trillion."

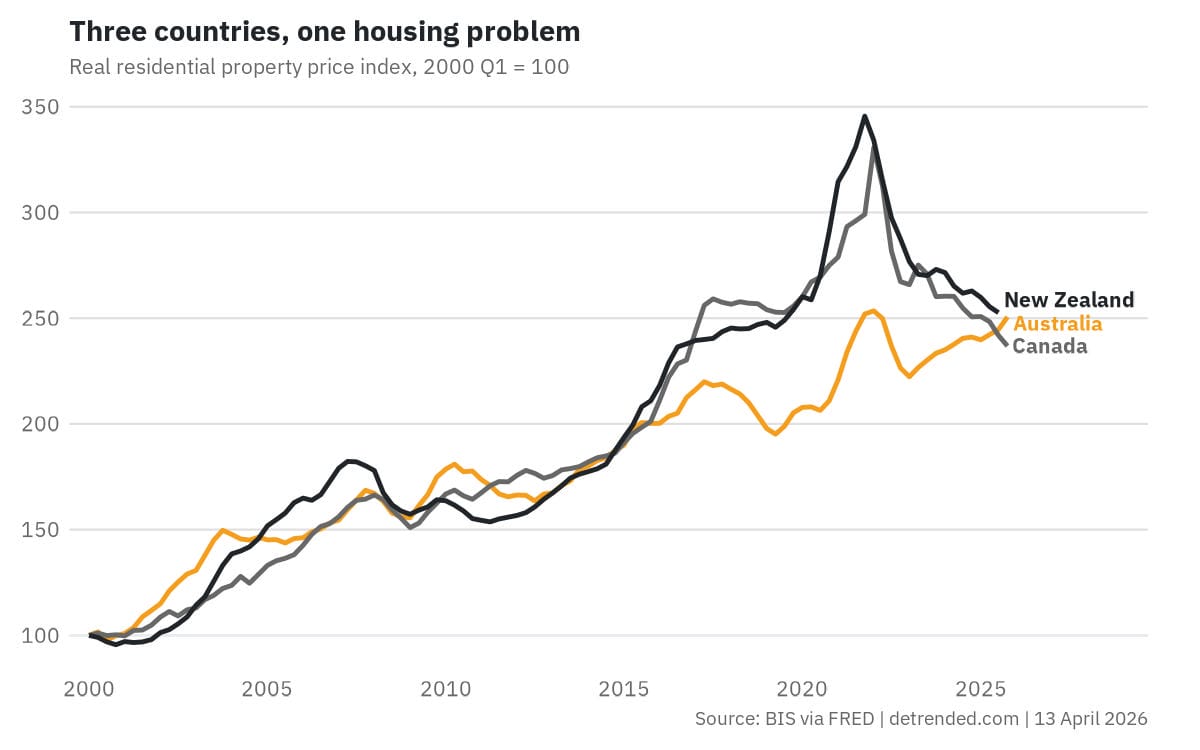

Schroder's comparison is good for shock value, but is only half right. It's true that the value of Australia's housing stock is around 4.4 times annual output, while in the US it's only 1.75 times. But those are two very different countries! The US aggregate ratio sits where it does because the likes of Houston, Phoenix, Dallas, and Atlanta exist: large, growing and productive cities where a median earner can still buy a detached house for roughly four times income.

Australia has no equivalent; it's basically what the US national data would look like if every city was in California or New York. Major cities in those high productivity states have a well-documented zoning-related supply problem, and Australia's are no different. That scarcity gets capitalised into land prices and shows up as housing "wealth" on the national balance sheet, but really it's just the present value of a policy-induced supply restriction, extracted by current owners from everyone who will need to live there in future.

Which brings me to Schroder's other main point:

"John Howard said nobody wants their house to drop in value.

For the last 25 years, all of our additional wealth has gone into inflated housing prices that you can't really do anything about because you've got to move from one house to another house."

Housing is wealth in an accounting sense, but not a welfare sense: the house is the asset; the shelter is the dividend. You don't get wealthier when the price rises because your cost of consuming that same dividend has risen by the exact same amount. We might want to consume more and nicer housing as we get wealthier, just as we like to drive better cars, but that has nothing to do with wealth creation.

Is it a problem that Australians pay so much for housing? Yes: it's a signal that the market for housing isn't functioning properly. But higher house prices don't necessarily come at the expense of productive investment; in a global market, there is no fixed lump of capital. The $12.3 trillion is a mark-to-market valuation of a planning constraint, and it exists only because the constraint exists.

So, what can be done? Schroder didn't offer a solution, other than that "we" need to "genuinely want housing to be a smaller proportion... of GDP" for it to happen.

Right. Except that's basically The Wizard of Oz thinking: click our heels together three times and hope for the best. It also doesn't even begin to address why the current "model" has persisted for so long, such as the misaligned incentives faced by those writing and benefiting from the rules and those who lose out.

Schroder does worry about bank stability, and that's a legitimate concern; a highly housing-levered financial sector would crater if house prices fell. While I think that's a separate conversation – if you're worried about the banks, use bank regulation such as requiring them to use more equity – it's still valid.

But the thing is, you don't necessarily need nominal house prices to fall for housing to be a smaller proportion of GDP. In fact, as Schroder's Howard quote makes clear, that's probably a political dead-end. But if you liberalise zoning rules and let construction catch up with demand, then real prices can still decline passively while nominal prices tread water. Incomes rise, mortgage serviceability improves, and debt-to-income ratios compress without anyone having to sell into a falling market.

That's also the only path that doesn't run straight through the banking system. Win, win, right?