Call it Jimflation

Australia's inflation is home brewed.

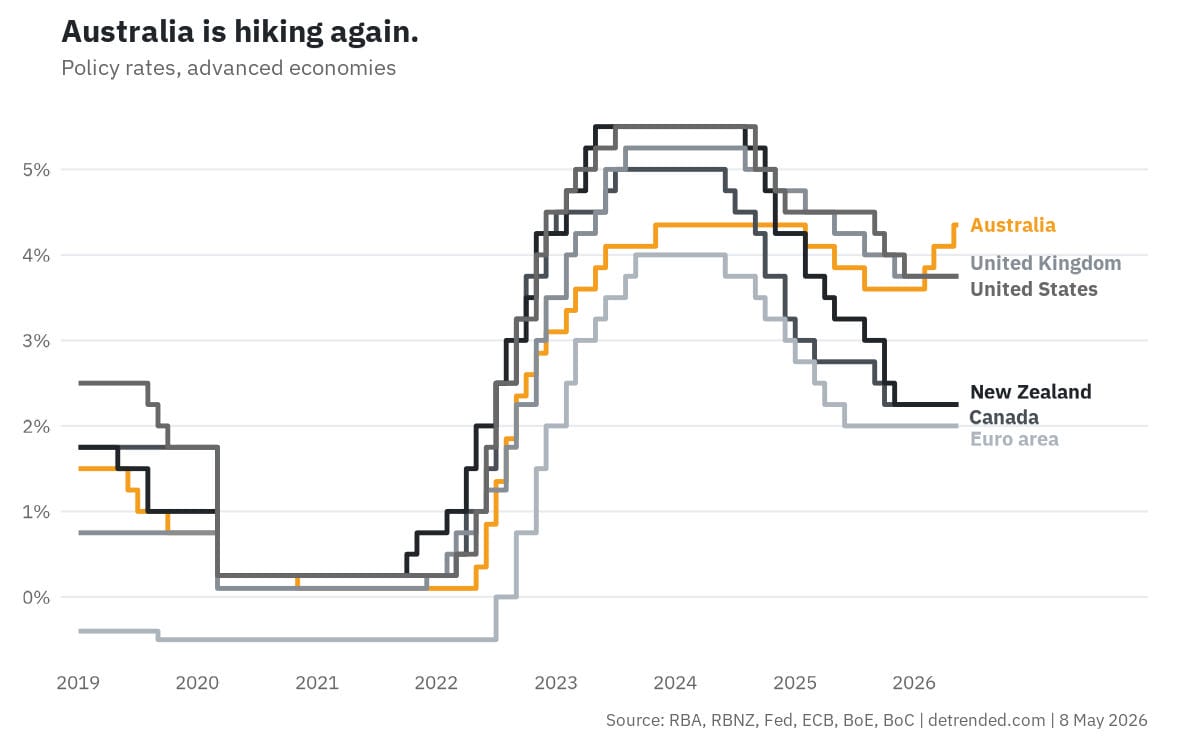

To no one's surprise, the Reserve Bank of Australia (RBA) raised interest rates again earlier this week. What's interesting is it was the third consecutive hike in a tightening cycle that commenced only six short months after the RBA's last rate cut. Australia is now well and truly a global outlier in the current cycle.

You might be tempted to blame the US war with Iran, as Treasurer Jim Chalmers did, for Australia's inflation woes:

"My job is to manage the Australian economy, and the Australian economy is getting absolutely pummelled by this war in the Middle East, and Australians are paying the price for that, and we're seeing that again today with this interest rate decision."

I suppose that means New Zealand somehow dodged the consequences of the war in Iran? Or perhaps there's another, more precise explanation.

The term "Jimflation" has been doing the rounds for a couple of years now, mostly from the usual suspects on the political right. It was too early back then: most of the Albanese government's early-term inflation was inherited and global, and the RBA's mistakes – trying to walk a "narrow path" – were (and still are) its own. But the case for the term has hardened with each passing month.

While the war in Iran added to measured inflation in March, actual inflation in Australia is predominantly home brewed. The structural deficit has widened, non-market sector employment is the dominant driver of jobs growth, and Commonwealth and state spending has been consistently expansionary since the pandemic.

Most of that fiscal profligacy sits on the Treasurer's desk. Yet after RBA governor Michele Bullock conceded that under present conditions government spending fuels inflation and necessitates tighter monetary policy ("it doesn't take much additional spending to make the job of returning inflation to target more challenging"), Chalmers responded:

"The governor was asked about that budget speculation in a hypothetical way, and gave a hypothetical answer."

Chalmers' answer was to dismiss the warning as a "hypothetical", refuse to rule out a $200-300 tax offset in next week's Budget in a follow-up question (precisely the kind of policy that makes the RBA's job more "challenging"), and gesture vaguely at "very substantial savings" elsewhere in a Budget he assured would be "one of the most responsible… in the last quarter-century or so".

In other words, he deflected any and all responsibility.

The problem with that is his government's spending has been a major contributor to Australia's persistent inflation problem. When households expect deficits to be partially financed by future inflation rather than repaid through real fiscal adjustment, inflation expectations rise and the central bank loses some control over the price level even with its policy rate set appropriately (which, in Jim's defence, it hasn't been). The mechanism doesn't require literal debt monetisation; it requires only that the public believes the government won't, when push comes to shove, choose unpopular fiscal restraint over inflation. Chalmers' performance this week is exactly the sort of signal that confirms that belief.

In a couple of weeks the Albanese government will have been in power for four years. Measured inflation has been above the RBA's target for... four years. While the early-term inflation was partly due to their predecessors, Chalmers' fingerprints are all over today's. By failing to provide a credible fiscal anchor, the Treasurer has chosen this rate of inflation. Call it Jimflation.