Why Western Australia is squandering generational wealth

And how to fix it for the future.

Australia's federal Budget is due to drop on Tuesday. A lot has been leaked but no one really knows what's going to be in it yet, so I'll wait until Wednesday before deciding whether to write a short post about it.

On the theme of Budgets, Western Australia's (WA) was released last week. WA is an interesting case because of the relatively outsized revenue it generates from mining royalties; iron ore alone contributed $8.8 billion to the bottom line this financial year, or around 16.7% of total state revenue.

You might think that with such an extreme amount of mining revenue flowing in, the WA government would be running large surpluses with no debt. Hell, you might be tempted to think that it would have a cashed-up sovereign wealth fund; a sort of rainy day stash of money invested globally in non-resource sectors to provide some kind of buffer against a commodity price crash.

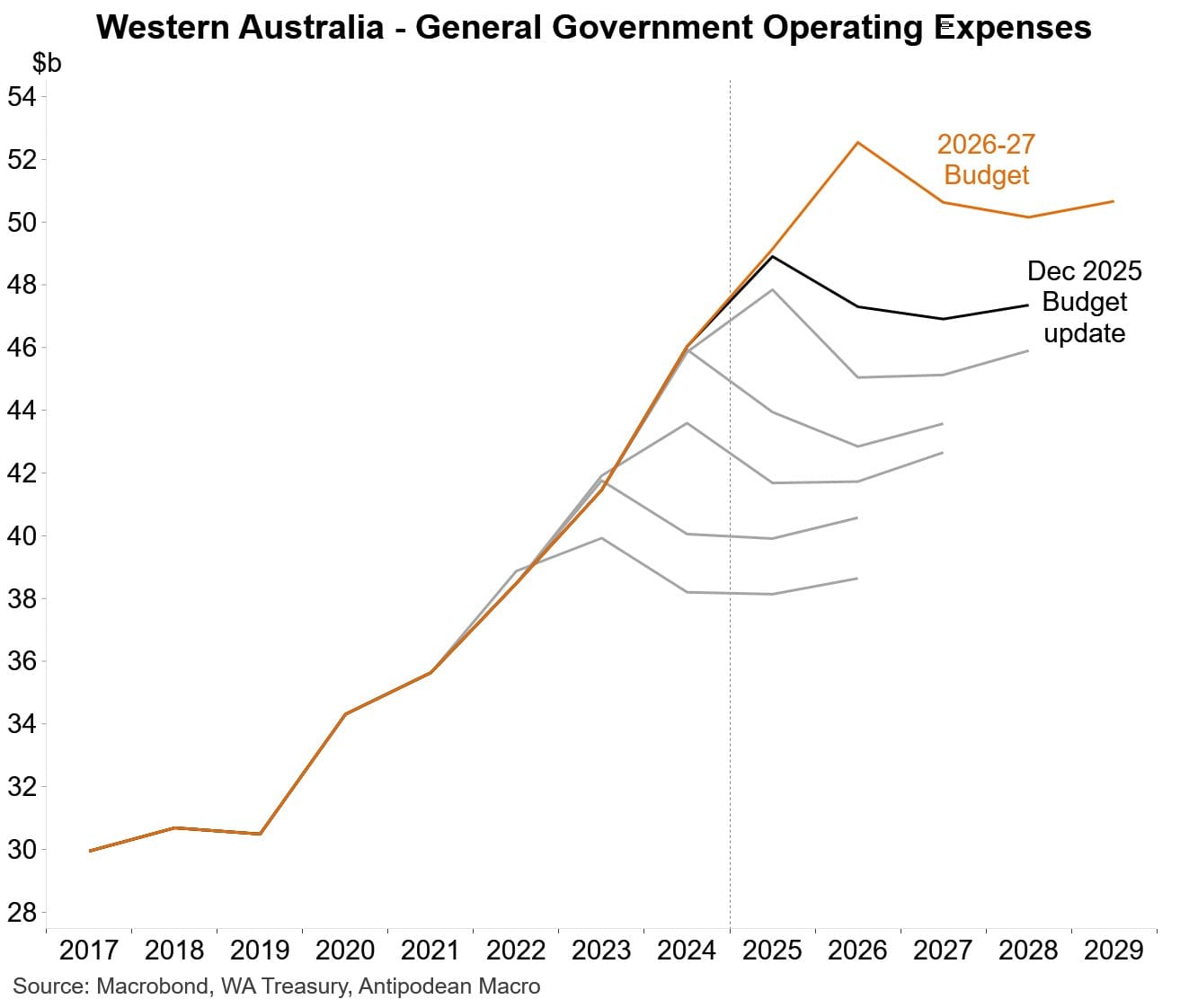

You would be wrong. While the headlines reported "another bumper surplus", the WA government as a whole (total non-financial public sector) is actually expecting to record a $5.8 billion cash deficit next financial year, after a $4.2 billion deficit this year. Its much-hyped surplus vanishes immediately when you add in all the spending they're increasingly hiding off-balance-sheet under the guise that it's "investment", although there's no regulatory requirement for it to earn a return. It's why net debt is expected to increase out to 2029.

So why is a state government, rolling in generational mineral wealth, squandering it so badly? One word: incentives.

Prior to 2018, WA's GST relativity bottomed out at 0.3 in 2015-16. What that meant was for every dollar of GST WA's population share entitled it to, the Commonwealth handed back just 30 cents. The system was equalising away the entire fiscal benefit of approving a mine. Mining carries real political and environmental costs, and a system that gives all the upside to states that wear none of those costs is one that disincentivises approving anything. The 2018 reforms, which implemented a floor of 75% of population share, with equalisation pegged to the stronger of NSW or Victoria, fixed a genuine problem.

But they also opened up a different can of worms. The current system pulls claimant states all the way up to the fiscal capacity of the standard state, defined as the fiscally stronger of NSW or Victoria. That's full insurance: if WA spends its boom into oblivion and iron ore craters, its GST relativity swings back within a couple of years and pulls the state back to par.

Equalisation, in other words, is now doing double duty as WA's diversification strategy. The state doesn't need a sovereign wealth fund because federation is the fund. Which is fine, except full insurance creates the moral hazard you'd expect: no fiscal cost to spending the boom because the bust will be socialised. Every time some extra royalty revenue flows in, they find a way to spend it immediately on something stupid like trying to fly AC Milan down to Perth.

There is a way to fix it: the floor on the revenue downside should be paired with a retention ceiling on the upside. Equalise claimant states up to, say, 80% of the benchmark rather than 100%. Donor states like boom-time WA would still subsidise genuine fiscal disability, but recipient states like bust-time WA would carry more of their own downside risk; skin in the game on both sides of the equation!

WA's Budget makes the case for such a reform: a state collecting $11 billion in royalties each year shouldn't be running a $6 billion cash deficit. That it can — and that the federation will catch it when iron ore prices turn — is the problem the 2018 reforms didn't solve, and is why there's so much persistent angst about it across Australia.